All Categories

Featured

Table of Contents

3Rider Insured's Paid-Up Insurance policy Acquisition Option in New York. 5Dividends are not ensured. Not all participating policy proprietors are qualified for dividends.

A term life policy offers a set quantity of protection for a time period that you select when you purchase it. That's the "term." It can range from 5, 10, also three decades.

Whole Life Insurance Online Instant Quote

We use cookies, APIs, and various other comparable technologies to recognize and assess your communications with our website. By using our site, you grant the usage of these technologies as defined in our Personal privacy Plan.

Selecting the quantity of life insurance policy and the length of time you need the coverage is key with term life. Depending upon your situations, you can choose insurance coverage to last for 1, 10, 15, 20 or three decades. Your costs stay the same for the term you select. If you pass away throughout the term and you have actually made all your costs settlements, the policy will pay money, called a fatality advantage, to the recipient of your policy.

Photo credit: iStock/KaeArt The market for life insurance coverage is one clouded by misconceptions. The first has to do with cost. Customers think life insurance policy costs nearly three times as long as it actually does, according to the life insurance policy research team LIMRA. That's a quite large space. Imagine, for instance, if consumers overestimated the cost of milk by a comparable quantity: at over $10 a gallon, several of us would certainly abandon the 2% and start putting orange juice over our grain.

Just behind that is the concern of intricacy. The range of life insurance policy alternatives is as huge as the vocabulary made use of to describe them: variable life insurance policy, global life insurance, variable universal life, term life, home loan life, lump sum, decreased paid-upand repeatedly. This is a difficult labyrinth to browse, and discouragement is usual.

Nobody, nevertheless, intends to get duped. Yes thank you for that handy example! In some ways, purchasing life insurance is a lot like purchasing an automobile. Both are investments that will be with you for years, and both cost you a fair amount of money. You might have a basic concept of what you want first, however unless you're a specialist (i.e.

Additionally, it can be difficult to tell the trustworthy experts from the sales people. Unless you have a trustworthy outside advisor (and they can be costly) you have little selection however to think what you're hearing. As with getting an automobile, the finest point you can do is arm yourself with a little bit of knowledge concerning the items you are considering.

Instant Insurance Life Quote Term

In this way, when it's time to purchase, you can be certain you're getting the best thing based on a notified life insurance coverage contrast. Just how much you spend for your life insurance policy will depend upon aspects consisting of personal information (like age and wellness) and plan types. An on the internet tool can provide instant life insurance coverage quotes so you can have an idea of what you will pay for what kind of protection.

We so happen to have one for you (what are the chances !?!) right at the top of this page. If you're looking for aid making some choices, we've obtained that for you, too. The most basic divide in the life insurance policy globe is that in between Term Life Insurance Policy and Permanent Life Insurance Policy.

The distinction is an issue of time: one (long-term) lasts for life, and the various other (term) lasts for a limited period, set at the start. Since permanent life insurance allows you to secure a price for the duration, it is generally a lot more expensive than a similar term policy.

Insurance policy holders can obtain versus the cash financial savings in their strategy, or utilize the financial savings to pay premiums. The main benefit of a long-term plan, nevertheless, is that it enables you to assure that, whatever happens to you for the rest of your life, you will be insured, as long as you continue making your repayments.

The benefit of a term plan is that it permits you to prepare your insurance coverage around life events. If, for instance, you have actually simply had a child, you can get 20-year term life insurance so that if something happens to you prior to your youngster leaves home, he or she will be dealt with.

Instant Whole Life Insurance

With a Return of Premium policy, the premiums you pay are set aside and returned to you in full at the end of your term, whereas a Level plan features no such guaranteeyour costs, once paid, are gone. For that reason, Return of Costs policies are the more pricey of the two.

Insurance policy companies would like to know exactly how most likely they are to pay out your insurance coverage quantity: the greater that likelihood, the greater your costs. That's why life insurance policy rates vary so widely by age. The older you are, the more you can expect to pay. Even though they largely consider the same variables, life insurance service providers can price estimate significantly different costs on similar plans.

Instant Online Whole Life Insurance Quotes

There are little and big firms, nationwide and regional insurance firms, each with its very own toughness and weak points. These are some points to think about, along with the actual prices, when taking a look at life insurance policy quotes. Image credit report: iStock/BraunS Definitely. To begin, let's discover some insurance for Jane. She's 25 years old, in superb health, and stays in beautiful Ocean City, New Jacket.

She chooses the very best policy for her would be a twenty years level term policy. At that coverage quantity, and with those specs, she can obtain a plan for in between $12 and $17 per month. And also, she's got choices: 9 different insurance coverage firms have a plan within that rate range, according to our Life insurance policy Quotes device over.

Dale is 60 years old, and he intends to be covered for the rest of his life. He remains in ordinary health and he smokes. He wants a benefit of $400,000 to go to his spouse and youngsters if anything takes place to him. His policy is mosting likely to set you back greater than Jane'ssomewhere in between $1,240 and $1,588, depending upon which company he chooses to purchase from.

Of all, he's older, less healthy and a smoker: all of these variables, in the eyes of an insurance business, make him much more pricey to cover. Secondly, he wants a permanent plan. While Jane just needed insurance coverage for the next two decades, Dale's policy could cover a much longer period than that.

Want to do one even more? He's 47 years old, is in excellent however not exceptional health, does not smoke and lives in the City by the Bay: San Francisco. He desires a 20-year plan with a coverage amount of $100,000, and he wants his premiums back at the end of the term.

His costs are a bit greater than Jane's because he's older, and he desires the money-back assurance of a Return of Costs plan. life insurance quotes online instant no medical exam. On the other hand, they're less than Dale's because Melvin is in healthiness and doesn't smoke. And also, he only wants coverage for the next 20 years, and for a much smaller amount than Dale

Instant Free Life Insurance Quotes

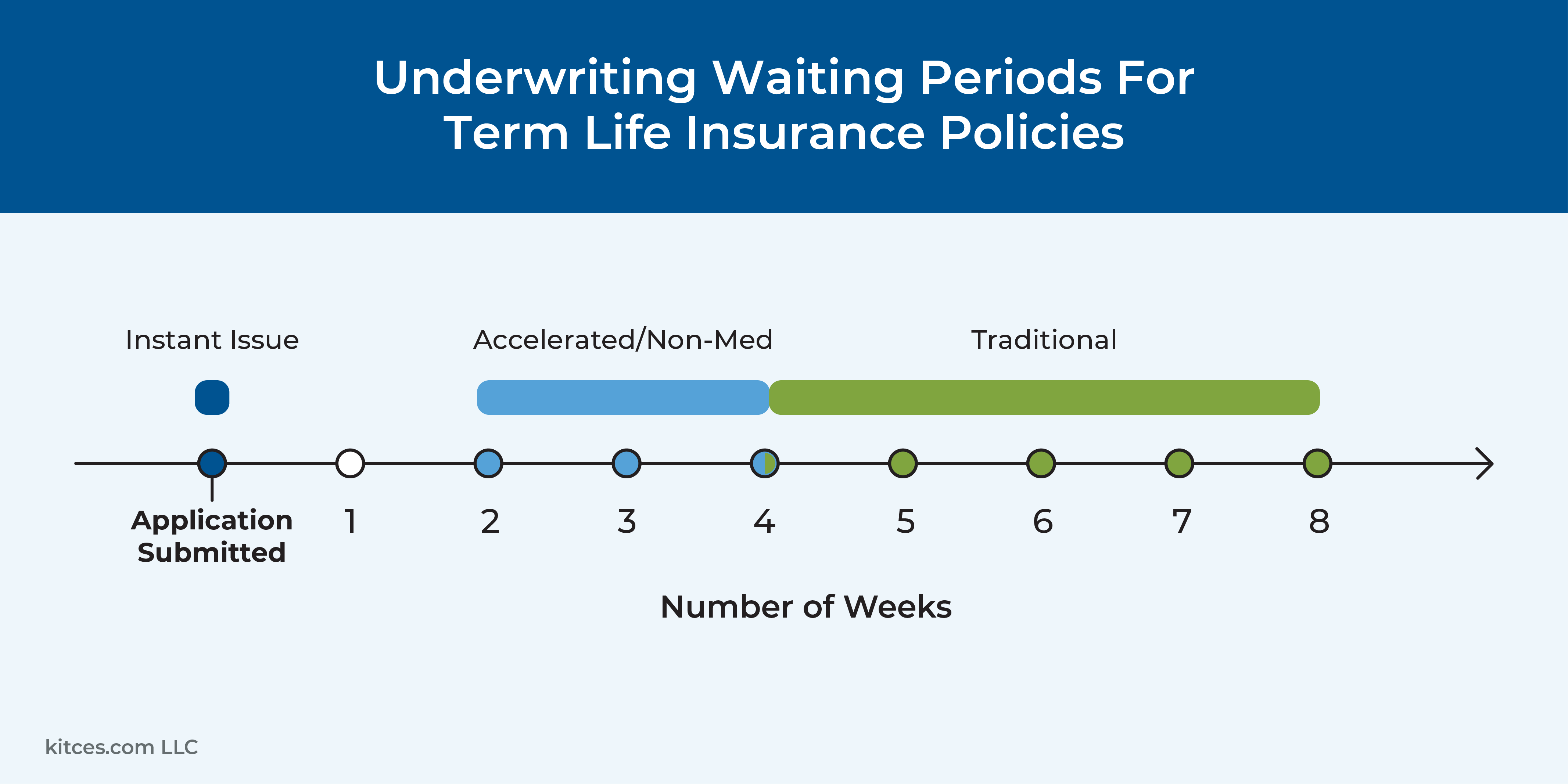

There's always strengths and weaknesses to whatever subject you're speaking about. How does this affect insurance? Well, that depends. See, each insurance company may have their own meaning of "immediate." Instant authorization term life insurance for one business will not be the same experience at another. For us at Wysh, immediate means that you can obtain protection within minutes of being confirmed by means of our underwriting procedure and authorizing your plan files.

Without an upgraded physical, the previous info is what will be used.: Without the medical exam, the benefit of an online life insurance application can't be understated. Whether you desire to use from your smart device or computer system, you can get your instant term life insurance coverage quote all without leaving the amazing side of your pillow.: Well, even more of a drawback.

{kind=link}

Latest Posts

Final Expense Life Insurance Plan

Final Expense Program

Top Ten Final Expense Companies